Personal tax measures - changes to pension tax thresholds and allowances

Lifetime Allowance (“LTA”)

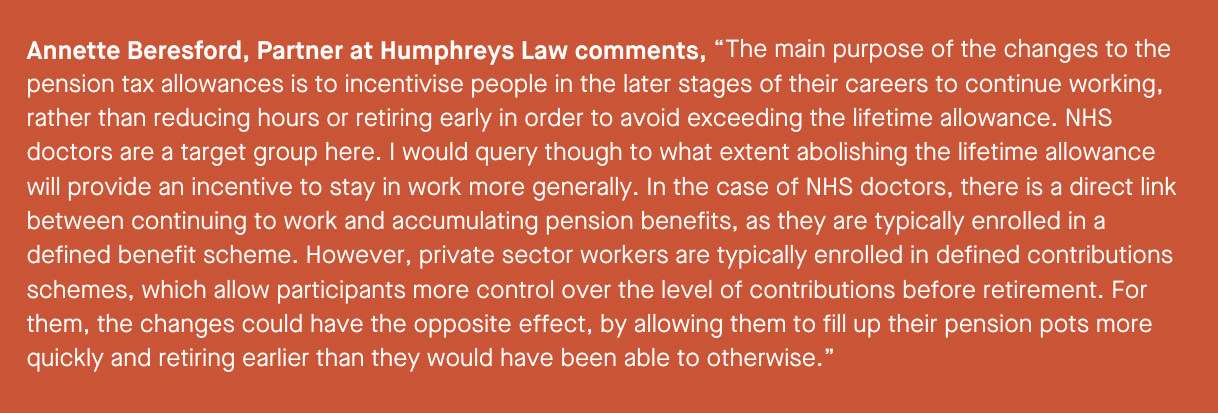

In a Budget aimed at getting people back to work, perhaps the biggest surprise was the abolishment (as opposed to a mere increase) of the Lifetime Allowance for tax-relieved pension savings.

Under current rules, where the LTA is exceeded, a charge is applied to the excess. The charge will either be 25% if the money is left in the pension pot, or 55% if the money is taken out of the pension pot. Introduced in April 2006 at £1.5 million, the LTA currently sits at £1,073,100 and has done since 2020/21 where it was expected to remain until 2025/26. However, it was thought that the LTA had an adverse effect on productivity by prompting people to reduce hours or retire early in order to avoid it.

The Chancellor has announced that the LTA charge will be removed from 6 April 2023 in the first instance, with legislation to abolish the LTA fully from 6 April 2024 being included in a future Finance Bill.

Pension Commencement Lump Sum

The maximum Pension Commencement Lump Sum, which refers to the maximum amount that an individual can take out of their pension pot as a tax-free lump sum, will be retained at its current level of £268,275 (for those who do not have any relevant protections allowing them to take a higher tax-free lump sum from previous rule changes) and will be frozen thereafter. Lump sums currently taxed for some individuals at 55% above the LTA will be taxed at an individual’s marginal rate of income tax. These measures will take effect from 6 April 2023.

Annual Allowance (“AA”)

As part of the back to work push and to further incentivise individuals to stay in work, the Chancellor also increased the limit of the AA from £40,000 to £60,000, again from 6 April 2023. The AA refers to the yearly limit in place on the amount of tax-relieved pension savings an individual can make in a year out of earnings.

Tapered Annual Allowance (“TAA”)

Introduced in April 2016, the TAA currently places further limits on the amount of tax relief that high earners can claim on their pension pots by reducing their AA to a minimum of £4,000. For the taper to apply, an individual must exceed the £200,000 limit of threshold income and the £240,000 limit of adjusted income. For every £2 of adjusted income over £240,000, an individual’s AA is reduced by £1.

Announced in the Spring Budget was an adjustment to the TAA, increasing the minimum allowance from £4,000 to £10,000. We also saw an increase in the adjusted income threshold at which the TAA kicks in from £240,000 to £260,000. Both of these changes to the TAA take effect from 6 April 2023.